Managing Credit Risks

Practical guidance for building effective credit risk management processes in your organization.

Foundation

What is credit risk management?

Credit risk refers to the likelihood of a customer's or borrower's failure to comply with the terms of a credit contract. Risk is shaped by internal factors — a company's solvency, profitability, and liquidity — and external factors such as industry shocks and macroeconomic changes. More information about risk assessment is presented on the Assessment Methods page.

Credit risk management encompasses the processes companies use to manage their receivables and borrowers. While it is central to banking and credit institutions, it applies broadly to any business selling on B2B credit. CreditReports.dk helps you perform efficient, data-driven credit risk estimation as part of that process.

Implementation

Tiered credit assessment approach

The scope of credit risk management typically depends on the number and variety of customers sold to on credit. Effective credit risk management uses a tiered approach, scaling the depth of assessment to the size of the credit decision:

Quick credit check

Small or medium-sized companies selling to a few clients can do well by simply checking credit ratings and some financials from the credit report. Our service offers three reports for free each month, and users can quickly check rating history, the proposed credit limit, and comparisons within the industry.

Suitable for: routine invoices, small credit amounts, existing low-risk customers

Deeper evaluation

Larger companies typically create processes based on credit amount so that once the amount exceeds a threshold (e.g. DKK 10,000 or DKK 100,000), a more thorough evaluation must be performed. Our reports provide comprehensive company information along with the possibility to create your own estimates, enabling thorough credit risk evaluation and sensitivity analysis.

Suitable for: medium credit amounts, new customers, elevated risk sectors

Senior authorization

For the largest credit decisions, C-suite authorization (CEO/CFO) is typically required. A full credit risk report — and potentially an AI Credit Report for written qualitative analysis — should be reviewed before approval.

Suitable for: large credit amounts, strategic customer relationships, high-risk situations

Example framework

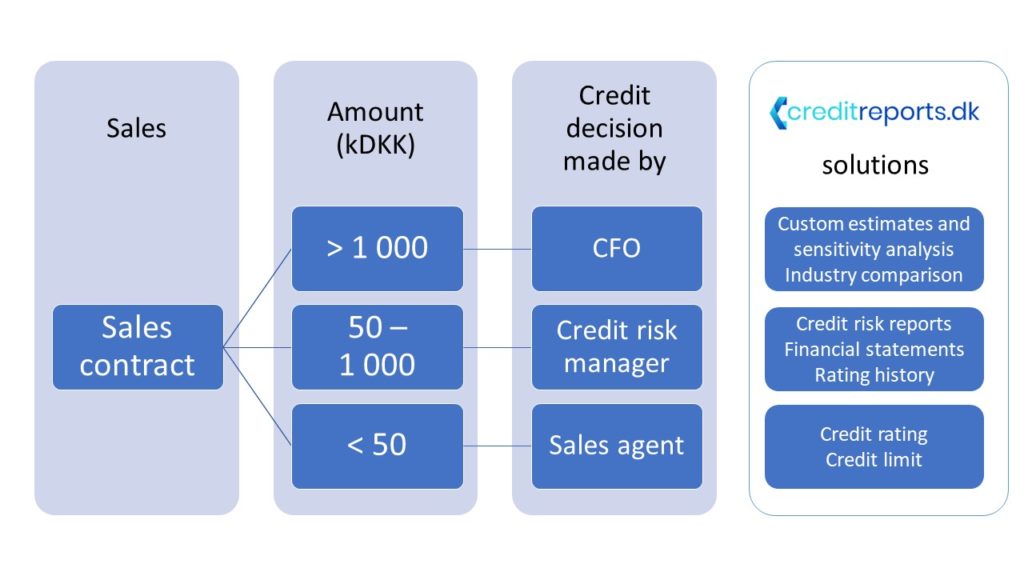

Three-level approval framework in practice

The image below illustrates one example of credit risk management in practice. A medium-sized company has three levels of approval for credit decisions on accounts receivables. If the invoice amount is small enough, an individual sales agent can make the decision after a quick check on rating and credit limit. For larger amounts, the credit decision is made by the risk manager or controller in the finance department. The largest credits are approved by the CEO or CFO. CreditReports.dk offers a variety of tools for each level of risk assessment.

Three-level approval structure

Level 1

Sales agents

Approve small invoices after a quick check on credit rating and credit limit in the platform

Level 2

Risk managers / controllers

Evaluate medium credit amounts with full report and scenario analysis

Level 3

C-suite (CEO/CFO)

Authorize the largest credit amounts after full review including AI-assisted written analysis

Need a decision-ready written analysis?

The AI Credit Report combines financial data with AI-assisted written analysis and qualitative observations — ideal for larger credit decisions that require more than raw numbers.

Learn about AI Credit Report